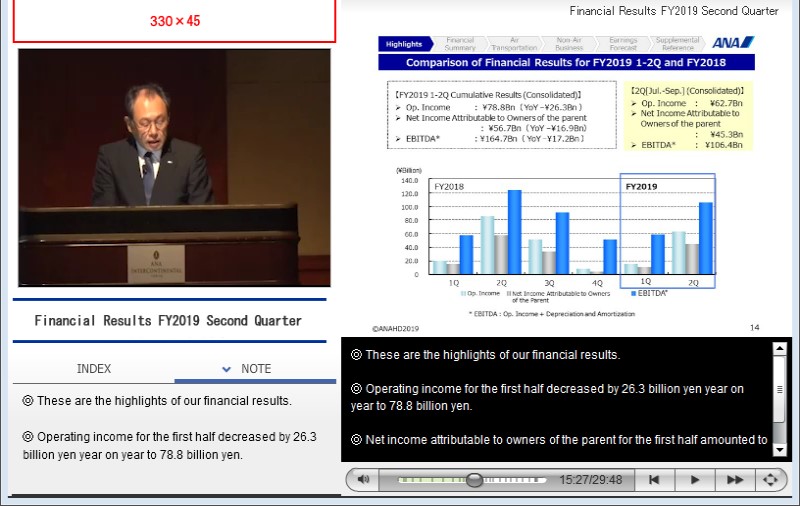

【ノート】

◎ Next, I will address our fiscal 2019 earnings forecast.

◎ Due to the deteriorating external environment, cargo demand on international routes continued to be sluggish. In addition, recent demand in our International Passenger Business was weaker than the first quarter.

Our LCC Business is experiencing intensifying competition from other companies in the industry. We expect this trend will continue throughout the second half of the fiscal year.

◎ In the midst of this environment, we have reviewed our financial results for the second quarter and conducted a careful study of our outlook for second-half operating revenues and expenses, deciding to make a downward revision in our forecast for the fiscal year.

◎ We now forecast operating revenue of 2,090 billion yen, 60 billion yen lower than our initial plan.

We are presently considering a revision to our operating expense projection; however, we have reduced our forecast for operating income by 25 billion yen compared to the initial plan of 140 billion yen.

Our updated forecast for ordinary income is 137 billion yen, while our forecast for net income attributable to owners of the parent is now 94 billion yen.

◎ We have left our forecast for dividends unchanged from our initial plan at 75 yen per share.

◎ Please turn to page 6.